%20Will%20Your%20Monthly%20Payment%20Go%20Up%20Under%20the%20New%20RAP%20Plan_.avif)

The One Big Beautiful Bill (OBBB) has introduced a significant change to federal student loans: the Repayment Assistance Plan (RAP), a new income-driven repayment (IDR) option.

However, RAP is not yet available. Its implementation is expected no earlier than July 2026, depending on how quickly federal agencies finalize regulations and build systems to deliver the program.

Until then, borrowers continue to use existing IDR plans such as Pay As You Earn (PAYE) and Income-Based Repayment (IBR). Understanding RAP now is important because it is expected to become the default and sole repayment option for new borrowers and for those who consolidate loans after July 1, 2026.

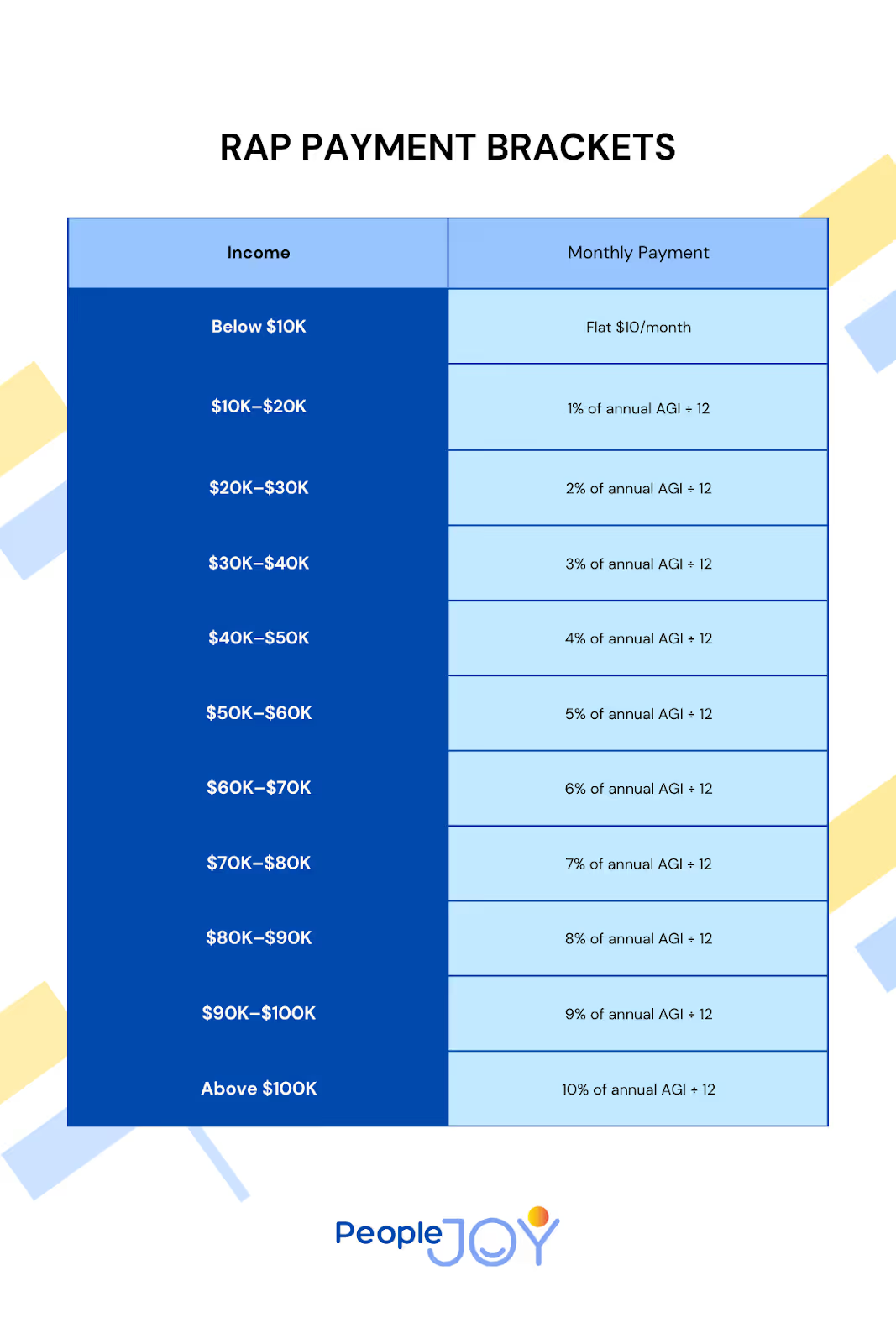

Overview of RAP Payment Structure

Under RAP, monthly payments are calculated using adjusted gross income (AGI) from the most recent tax year. The payment rates increase with income, as shown below:

Borrowers can reduce the calculated payment by $50 per dependent per month (based on tax return claims).

For comparison:

- SAVE plan: 5% of discretionary income for undergraduate loans, 10% for graduate loans; excludes 225% of the federal poverty line from the calculation.

- Old IBR: 15% of discretionary income; 150% poverty line exclusion.

- New IBR: 10% of discretionary income; same 150% exclusion.

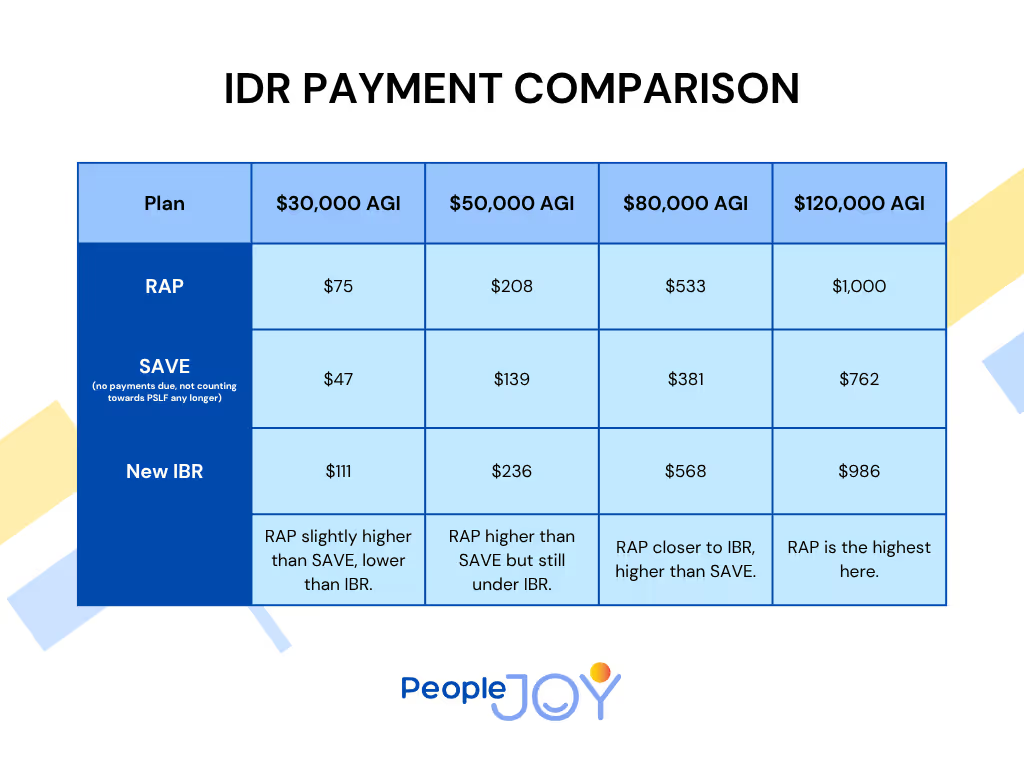

Example Payment Comparison

Below is a table showing estimated monthly payments at different income levels for a single borrower with undergraduate loans:

Why RAP May Lead to Higher Payments

The main reason RAP can result in higher monthly payments is its use of total AGI without adjusting for poverty levels. In contrast, SAVE and IBR plans apply poverty-line deductions, which reduce the amount considered in the payment calculation.

Furthermore, while RAP offers a fixed dependent deduction ($50 per child per month), SAVE and IBR use family size to adjust the poverty exclusion more dynamically — often benefiting larger households.

Who Could Benefit, and Who Might Pay More

Groups that may benefit from RAP:

- Borrowers with low incomes

- Households with multiple dependents

- Borrowers pursuing Public Service Loan Forgiveness (PSLF), which offers cancellation after 10 years

Groups that may face higher payments:

- Middle- and high-income borrowers

- Borrowers currently eligible for SAVE’s 5% rate on undergraduate loans

- Married borrowers filing jointly where one partner has significantly higher income

Important Note: RAP Is Not Yet Available

RAP is not currently an active repayment option, and it will not be available until at least mid-2026. Borrowers making repayment decisions today will need to continue under existing IDR plans.

In addition, after July 1, 2026, those who take out new federal loans or consolidate existing loans may have no option but to repay under RAP.

Recommendations Before RAP Launches

Before making any decisions about loan repayment:

- Use an updated IDR calculator to estimate payments under current plans.

- Review tax filing strategies, such as whether filing separately would reduce household payment calculations.

- Seek professional advice or counseling to understand long-term impacts, especially for those considering consolidation.

Final Takeaway

RAP may provide meaningful relief for some borrowers but could lead to higher monthly payments, especially for middle- and upper-income earners. As implementation is still years away, borrowers are encouraged to make informed decisions under the current system and avoid assuming that RAP will offer immediate solutions.