%20Stuck%20in%20Student%20Loan%20Default_%20Here%E2%80%99s%20How%20to%20Get%20Back%20on%20Track.avif)

Defaulting on your federal student loans can feel like being trapped in a financial nightmare 😟. Your credit takes a hit, your wages could be garnished, and suddenly, the dream of financial independence feels out of reach. But here’s the truth many don’t realize: you’re not stuck forever—and you have clear, actionable options to recover fast.

Whether you’re hearing from collection agencies or just found out your loans have entered default, this blog is your roadmap to recovery. Let's walk through the fastest, most effective ways to get out of default and back into good standing.

Understanding Student Loan Default

Your federal student loan goes into default when payments are more than 270 days past due. The consequences are serious:

- Credit score damage

- Loss of federal benefits (like deferment, forbearance, and income-driven repayment plans)

- Wage garnishment and tax refund seizure

- Collection fees and penalties

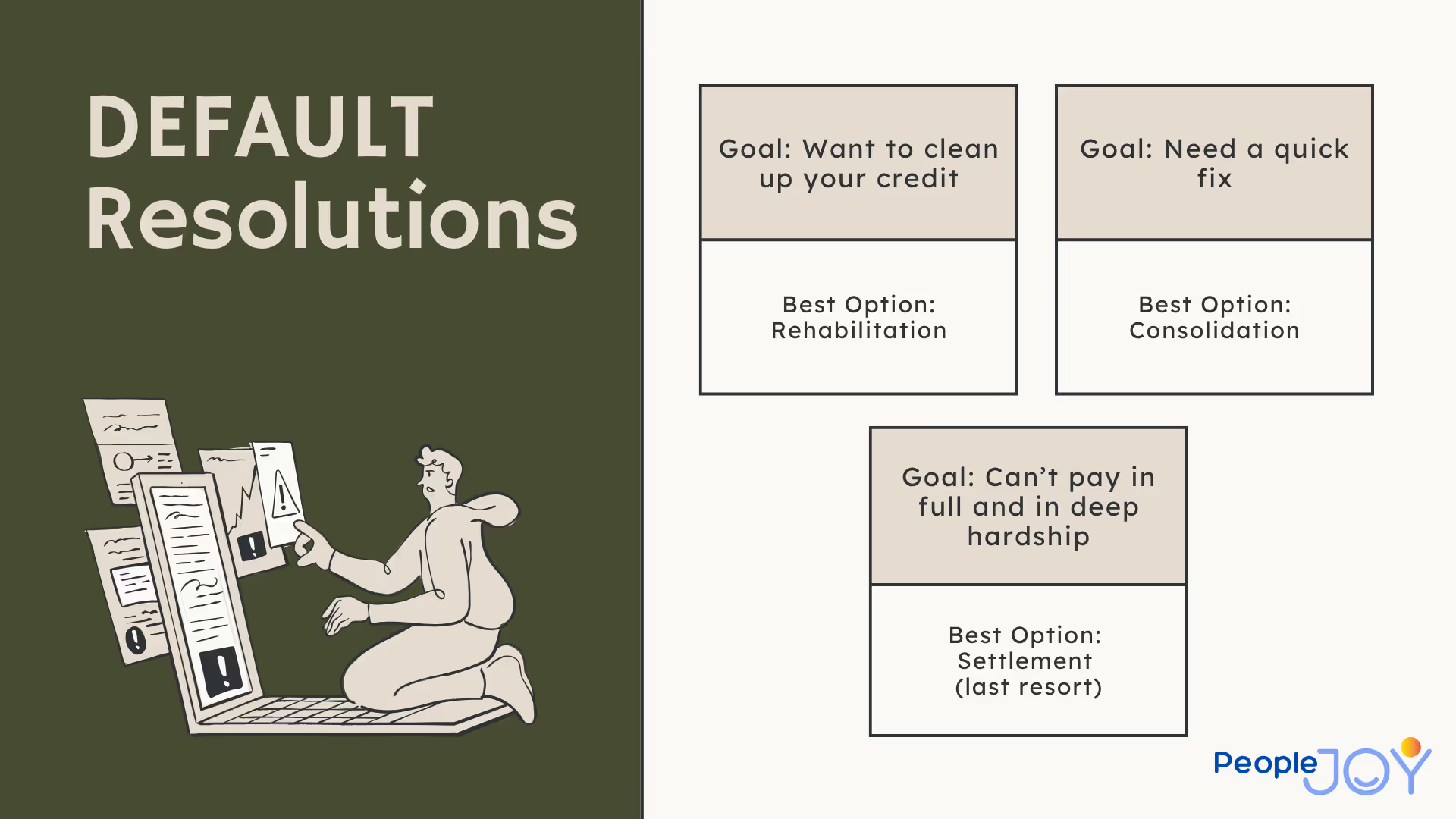

But there’s good news: the U.S. Department of Education offers three clear pathways to get out of default: Loan Rehabilitation, Loan Consolidation, and, in limited cases, Settlement.

Let’s break them down.

1. Loan Rehabilitation: The Fresh Start Route 🔁

Loan rehabilitation is often the most beneficial long-term solution. It lets you:

- Remove the default status from your credit report

- Regain eligibility for federal benefits

- Avoid collections and wage garnishment

👉 How it works:

You agree to make nine consecutive, affordable monthly payments—based on your income—within 10 months.

Pros:

- Default status removed from your credit report

- Keeps your existing loans intact

- Restores access to IDR plans and forgiveness programs (like PSLF)

Cons:

- Takes time (minimum 9–10 months)

- Can only be used twice per loan

2. Loan Consolidation: The Fast Track Option 🚀

If you want out of default now, consolidation is your fastest option.

Here’s what happens:

You apply to combine your defaulted loan into a new Direct Consolidation Loan. To qualify, you must agree to:

- Repay the new loan under an income-driven repayment (IDR) plan, or

- Make three consecutive voluntary payments on the defaulted loan first

Pros:

- Immediate exit from default

- Restores access to repayment plans and forgiveness

- Stops wage garnishment (after processing)

Cons:

- Doesn’t remove the default mark from your credit report

- Loan balance may increase slightly with added interest

Still, for many, this is the quickest and cleanest path forward.

3. Loan Settlement: The Rare Last Resort 💸

Settling your federal loan—paying less than the full amount owed—is possible, but it’s uncommon and tricky.

You’ll typically need to:

- Prove long-term financial hardship

- Negotiate with the collection agency or U.S. Department of Education

- Pay a lump sum

Pros:

- Can reduce what you owe

- Resolves the default

Cons:

- Rarely approved

- Must pay in full immediately

- Default status stays on your credit report

- You lose federal aid eligibility unless you consolidate or rehabilitate later

Bottom line? Settlements are often a last resort for those unable to pursue rehabilitation or consolidation.

Which Option Is Best for You?

😌 Remember: Getting out of default isn’t just about resolving your loan—it’s about regaining your financial peace of mind. And yes, you deserve that.

💼 Why Getting Out of Default Matters for Forgiveness Programs

One of the most overlooked benefits of getting your federal student loans out of default is this:

➡️ Once your loans are no longer in default, they become eligible for critical forgiveness programs like:

- Public Service Loan Forgiveness (PSLF)

- Income-Driven Repayment (IDR) Forgiveness

- Teacher Loan Forgiveness

- Closed School Discharge and Borrower Defense to Repayment

Defaulted loans are not eligible for these programs. That means every month your loan remains in default is a month lost toward forgiveness.

But once you rehabilitate or consolidate your loans and enter an eligible repayment plan, the countdown to forgiveness can begin—especially if you work in public service, education, or nonprofit healthcare. You can also regain access to deferment, forbearance, and subsidized interest benefits.

🏥 If you’re a teacher, nurse, nonprofit worker, or government employee, getting out of default isn’t just about relief—it’s a direct path to forgiveness. Don't let default delay your financial freedom.

What Comes Next: Take the First Step Today 💪

Dealing with student loan default is overwhelming—but now, you’re informed. Whether you choose to rehabilitate or consolidate, the most important step is starting.

🎯 And if your employer offers access to student loan support through PeopleJoy, you might already have expert help on your side. Not sure if they do? Ask your HR team today!

💡 Don’t have PeopleJoy at your workplace?

We help borrowers get out of default, qualify for loan forgiveness, and reclaim their financial futures every day.

📣 Let your HR team know about PeopleJoy and how we can support you—and your coworkers—through every step of the student loan journey.