%20How%20Long%20Does%20It%20Take%20to%20Fix%20a%20Student%20Loan%20Default%E2%80%94And%20How%20Will%20You%20Know%20When%20It%E2%80%99s%20Resolved.avif)

Falling into default on your federal student loans can feel overwhelming, but getting back into good standing is often faster and more straightforward than many borrowers expect. Whether you’ve just defaulted or have been in default for a longer period, there are clear steps that can help you stop collections, rebuild eligibility, and move forward with confidence.

Below is a simple, borrower-friendly guide on how long it takes, what your options are, and how you’ll know the process is complete.

Recently Defaulted Loans: The Quickest Path Back to Good Standing

Borrowers who defaulted within the last several months usually have the fastest recovery timeline.

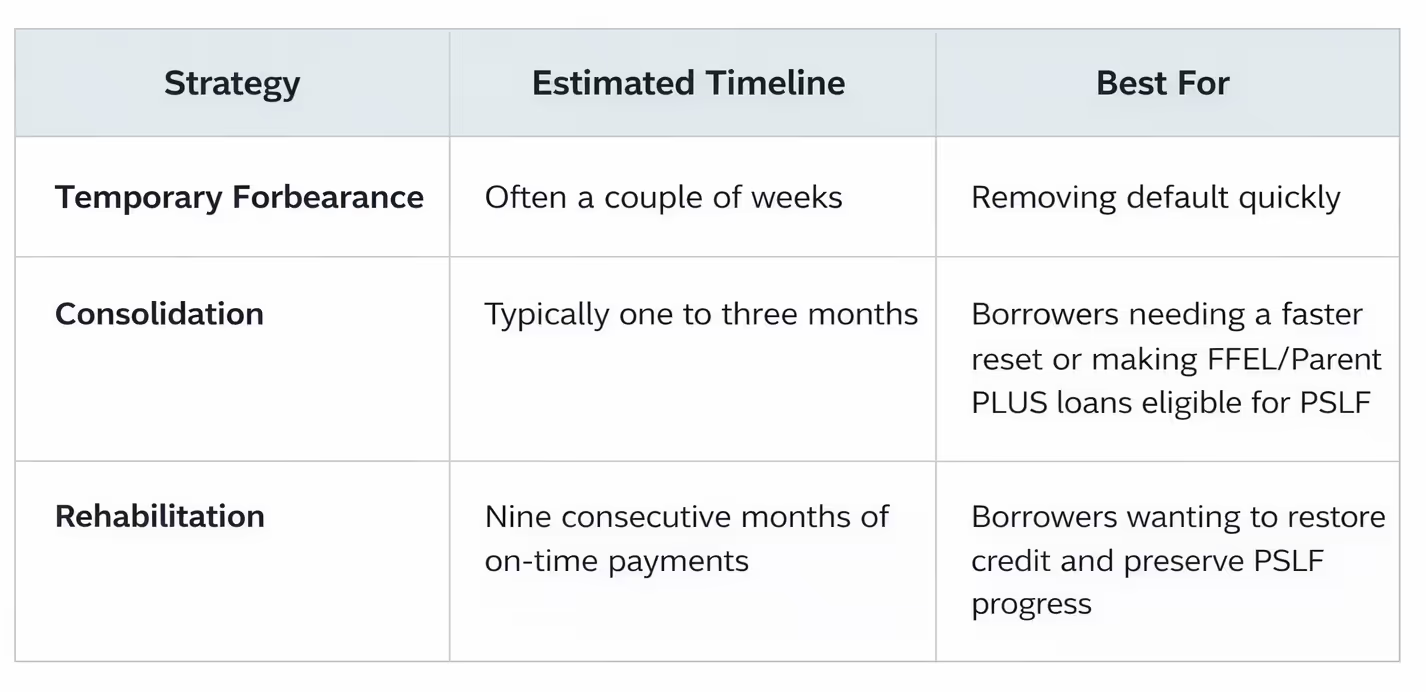

Request a Temporary Forbearance

Calling your servicer to request a temporary forbearance is often the quickest way to halt collections activity. Most borrowers have up to 36 months of forbearance over the life of their loan.

Typical result:

This step can stop wage garnishment and pull your loan out of default within a couple of weeks.

Submit an Income-Driven Repayment (IDR) Application

You can also apply for an IDR plan, which sets your payment based on your income. PeopleJoy can help prepare and submit this application, including income documentation. IDR processing usually takes around a month, though it may take longer depending on servicer volume.

Longer-Term Default: Your Options Depend on Loan Type and PSLF Progress

If your loan has been in default for a longer period, your recovery path generally depends on:

- Your loan type (Direct, FFEL, Parent PLUS)

- Whether you have earned PSLF credit

- Whether preserving PSLF months is important to you

At this stage, borrowers typically move forward using either consolidation or rehabilitation, and the best option varies based on your situation.

Consolidation or Rehabilitation (Depends on Your Eligibility)

Both options can restore your loan to good standing, but the right choice depends on your goals:

- If maintaining PSLF credit is important, rehabilitation may be more beneficial.

- If you want a faster reset, consolidation may be the better fit.

- If you have FFEL or Parent PLUS loans, consolidation is often the key step that unlocks PSLF eligibility. (*Eligibility for Parent Plus Loans will change in July 2026!)

- If you’ve already earned PSLF months prior to defaulting, the path you choose can affect whether those months are preserved.

PeopleJoy helps borrowers understand which option aligns with their loan type, repayment goals, and PSLF progress.

How You’ll Know Your Default Is Resolved

No matter which path you take, you’ll know your default has been corrected when:

✔ Collections activity stops

This includes wage garnishment, tax refund offsets, and collection calls.

✔ Your loan status updates online

Your servicer dashboard should show your loans as “current,” “in repayment,” or “consolidated.”

✔ You receive official confirmation

Servicers typically send a letter or email confirming your new repayment status.

✔ Your credit report reflects the change

If you complete rehabilitation, the default status is removed entirely.

How Long the Process Usually Takes

You Don’t Have to Do This Alone

Restoring your loans to good standing is absolutely achievable—and often faster than expected—but choosing the right path can be confusing, especially when PSLF credit and loan type come into play.

PeopleJoy supports borrowers with:

- Contacting loan servicers

- Assessing your PSLF history

- Submitting IDR, consolidation, or rehabilitation forms

- Ensuring you're placed in the correct repayment plan afterward

If you're in default, we're here to guide you through every step and help you get back on track with confidence.